Lasso and Ridge Regression

These are my notes for Lasso (L1 Regularization) and Ridge (L2 Regularization). I would highly recommend checking out the following resources (that I utilized)

- Intro to Statistical Learning with Applications in R

- Statquest Lasso Regression

- Statquest Ridge Regression

- Statquest Ridge vs Lasso Regression, Visualized

Lasso Regression

Lasso regression minimizes the following equation:

MSE + lambda * np.abs(coef)

Lambda can be between 0 and positive infinity and lets the equation know how much to weight the lasso component of the formula.

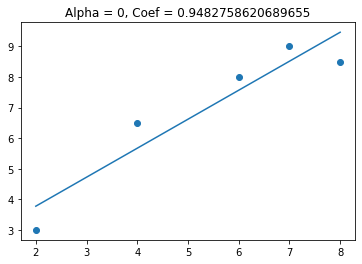

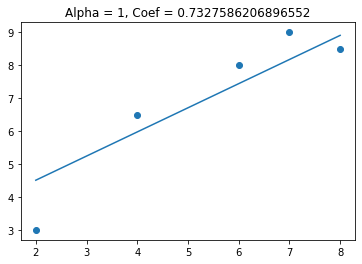

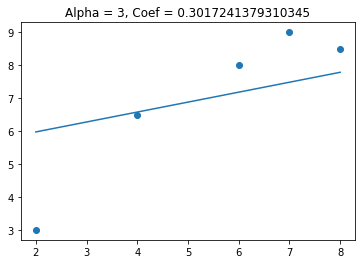

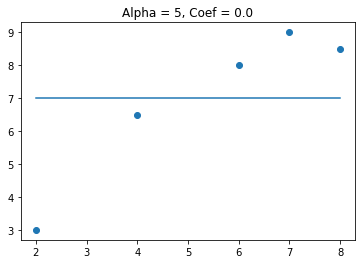

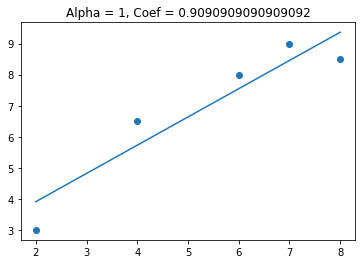

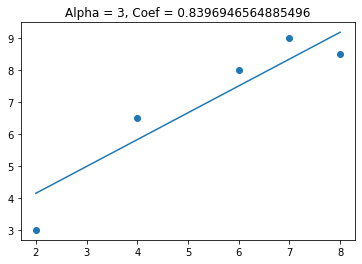

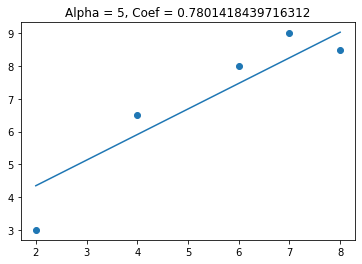

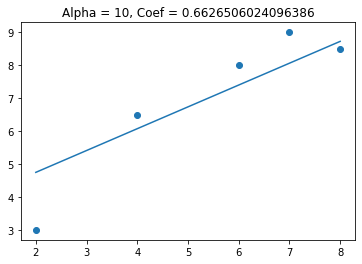

I’m going to create a dataset and see how my line changes as lambda increases.

import pandas as pd

import matplotlib.pyplot as plt

from sklearn.linear_model import Lasso

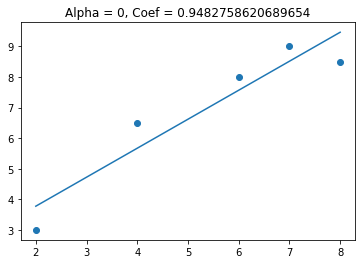

df = pd.DataFrame({'x': [2, 4, 6, 7, 8], 'y':[3, 6.5, 8, 9, 8.5]})

for i in [0, 1, 3, 5, 10]:

lasso = Lasso(alpha=i)

lasso.fit(df['x'].values.reshape(-1, 1), df['y'])

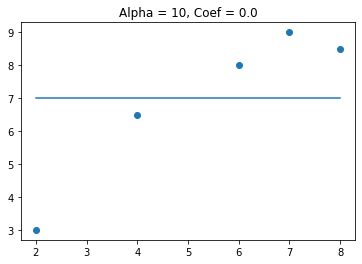

plt.scatter(df['x'], df['y'])

plt.plot(df['x'], lasso.predict(df['x'].values.reshape(-1, 1)))

plt.title(f'Alpha = {i}, Coef = {lasso.coef_[0]}')

plt.show()

We see that when alpha gets above 3 the coefficient goes to zero. This can be useful when I have features that are not needed for predicting the target variable. Lets see what happens when I add a feature that is not useful in predicting the target variable.

# create random variable

import numpy as np

np.random.seed(9)

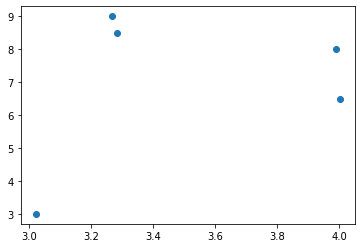

df['x1'] = np.random.uniform(3, 5, 5)

# plot out new feature

plt.scatter(df['x1'], df['y']);

We see there is not a linear relationship between the x1 and y. Lets see how the coefficients changes as lambda increases.

x_coef = []

x2_coef = []

for i in [0, 1, 3, 5, 10]:

lasso = Lasso(alpha=i)

lasso.fit(df[['x', 'x1']], df['y'])

x_coef.append(lasso.coef_[0])

x2_coef.append(lasso.coef_[1])

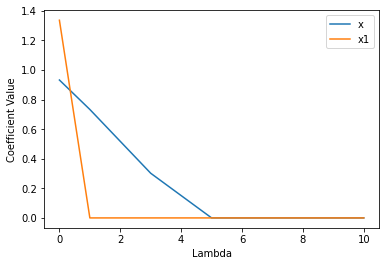

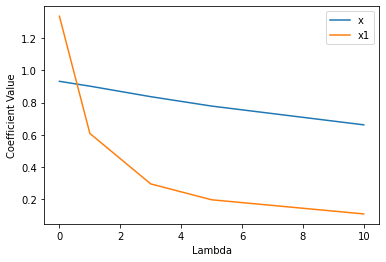

plt.plot([0, 1, 3, 5, 10], x_coef, label = 'x')

plt.plot([0, 1, 3, 5, 10], x2_coef, label = 'x1')

plt.legend()

plt.xlabel('Lambda')

plt.ylabel('Coefficient Value')

We see that x2 goes to zero much quicker than x, this is because x is a useful feature and x2 is not.

When using lasso regression, we need to find the best parameter for the lambda. I am going to do that using LassoCV

from sklearn.linear_model import LassoCV

lassocv = LassoCV()

lassocv.fit(df[['x', 'x1']], df['y'])

lassocv.alpha_

0.02042299086789623

We see that the optimal value of lambda is 0.02. Now I am going to look at Ridge Regression

Ridge Regression

Lasso regression minimizes the following equation:

MSE + lambda * coef**2

Lambda can be between 0 and positive infinity and lets the equation know how much to weight the lasso component of the formula.

Again I am going to look at the slope as lambda changes

from sklearn.linear_model import Ridge

for i in [0, 1, 3, 5, 10]:

ridge = Ridge(alpha=i)

ridge.fit(df['x'].values.reshape(-1, 1), df['y'])

plt.scatter(df['x'], df['y'])

plt.plot(df['x'], ridge.predict(df['x'].values.reshape(-1, 1)))

plt.title(f'Alpha = {i}, Coef = {ridge.coef_[0]}')

plt.show()

This time we see that the coefficient gets smaller, but doesn’t get to zero. Lets see what happens to the coefficients when I have 2 variables in my model (one useful and one not useful).

x_coef = []

x2_coef = []

for i in [0, 1, 3, 5, 10]:

ridge = Ridge(alpha=i)

ridge.fit(df[['x', 'x1']], df['y'])

x_coef.append(ridge.coef_[0])

x2_coef.append(ridge.coef_[1])

plt.plot([0, 1, 3, 5, 10], x_coef, label = 'x')

plt.plot([0, 1, 3, 5, 10], x2_coef, label = 'x1')

plt.legend()

plt.xlabel('Lambda')

plt.ylabel('Coefficient Value')

This time we see that x goes down slightly while x1 decreases more significantly. This makes sense because x1 is not useful.

Like Lasso Regression, I need to find the optimal value of lambda for ridge regression.

from sklearn.linear_model import RidgeCV

ridgecv = RidgeCV()

ridgecv.fit(df[['x', 'x1']], df['y'])

ridgecv.alpha_

1.0

Comparison of Lasso and Ridge Regression

Now I am going to compare the performance of Lasso and Ridge Regression

from sklearn.datasets import make_regression

X, y = make_regression(n_samples = 1000, n_features = 100, n_informative=10, random_state=11, noise = 20)

I have 1000 rows, 100 predictors, with only 10 of them informative. Lets see whether Lasso, Ridge, or Linear Regression does best.

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.25, random_state=11)

Start with Linear Regression

from sklearn.linear_model import LinearRegression

lr = LinearRegression()

lr.fit(X_train, y_train)

# calculate MSE

from sklearn.metrics import mean_squared_error

lr_mse = mean_squared_error(y_test, lr.predict(X_test))

print(lr_mse)

457.0964335435198

lassocv = LassoCV()

lassocv.fit(X_train, y_train)

lasso_mse = mean_squared_error(y_test, lassocv.predict(X_test))

print(lasso_mse)

404.06019286558563

ridgecv = RidgeCV()

ridgecv.fit(X_train, y_train)

ridge_mse = mean_squared_error(y_test, ridgecv.predict(X_test))

print(ridge_mse)

456.85177007126435

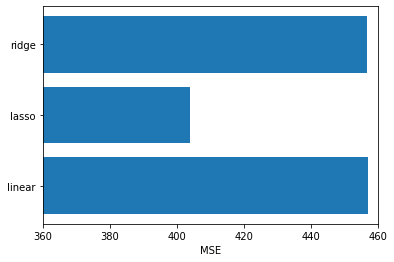

plt.barh(y = ['linear', 'lasso', 'ridge'], width = [lr_mse, lasso_mse, ridge_mse])

plt.xlim([360, 460])

plt.xlabel('MSE');

We see that lasso regression has the lowest MSE. This is because there are 100 features and only 10 of them are useful. Lasso regression is removing a lot of those non-useful features and giving them a 0 coefficient.

f'Lasso used {np.sum(lassocv.coef_ != 0)} features'

'Lasso used 35 features'

f'Ridge used {np.sum(ridgecv.coef_ != 0)} features'

'Ridge used 100 features'

Lasso regression can be used as a feature selection technique. Lets use the features that Lasso selected and use it with ridge regression.

df_train = pd.DataFrame(X_train)

df_test = pd.DataFrame(X_test)

lasso_df_train = df_train.loc[:, lassocv.coef_ != 0]

lasso_df_test = df_test.loc[:, lassocv.coef_ != 0]

ridgecv = RidgeCV()

ridgecv.fit(lasso_df_train, y_train)

ridge_mse_with_lasso = mean_squared_error(y_test, ridgecv.predict(lasso_df_test))

plt.barh(y = ['linear', 'lasso', 'ridge', 'ridge_with_feature_selection'],

width = [lr_mse, lasso_mse, ridge_mse, ridge_mse_with_lasso])

plt.xlim([360, 460])

plt.xlabel('MSE');

We see that using the feature selection improved the performance of the ridge regression, but lasso regression is still the best performing model.

Now lets see what happens if we make a small dataset and all the features are informative.

X, y = make_regression(n_samples = 50, n_features = 10, n_informative=10, random_state=11, noise = 10)

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.25, random_state=11)

lr = LinearRegression()

lr.fit(X_train, y_train)

# calculate MSE

from sklearn.metrics import mean_squared_error

lr_mse = mean_squared_error(y_test, lr.predict(X_test))

print(lr_mse)

61.76711409271062

lassocv = LassoCV()

lassocv.fit(X_train, y_train)

lasso_mse = mean_squared_error(y_test, lassocv.predict(X_test))

print(lasso_mse)

59.06356274259228

ridgecv = RidgeCV()

ridgecv.fit(X_train, y_train)

ridge_mse = mean_squared_error(y_test, ridgecv.predict(X_test))

print(ridge_mse)

57.86644722800123

plt.barh(y = ['linear', 'lasso', 'ridge'], width = [lr_mse, lasso_mse, ridge_mse])

plt.xlim([55, 65])

plt.xlabel('MSE');

Now we see that Ridge Regression is the best performing model. This makes sense because all the features are useful.

Why does Lasso have 0 coefficients but Ridge does not?

I am going to use my original dataset that I have below.

df = pd.DataFrame({'x': [2, 4, 6, 7, 8], 'y':[3, 6.5, 8, 9, 8.5]})

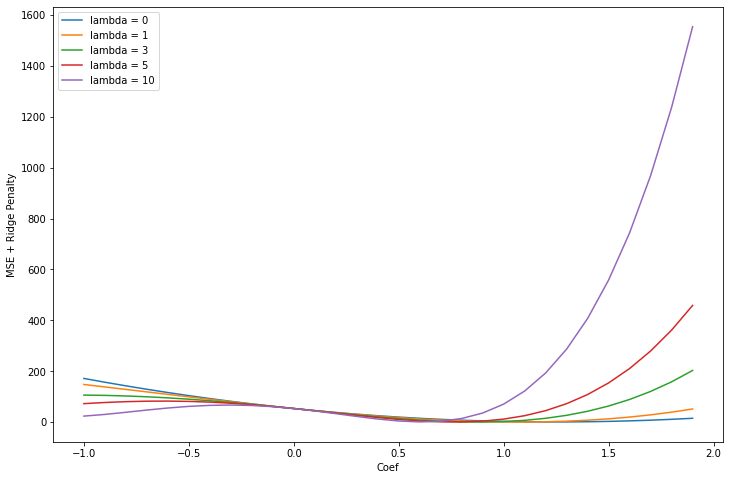

Next I am going to try see what the optimum coefficient level for each lambda. I am going to do this by plotting coefficient along the x axis and the MSE + Ridge Penalty is at the different lambda levels.

plt.figure(figsize = (12, 8))

for lam in [0, 1, 3, 5, 10]:

mse = []

for i in np.arange(-1, 2, .1):

mse.append(mean_squared_error(df['y'], df['x'] * i + (lam * (i **2))))

plt.plot(np.arange(-1, 2, .1), mse, label = f'lambda = {lam}')

plt.legend()

plt.ylabel('MSE + Ridge Penalty')

plt.xlabel('Coef');

I see that as lambda increases the minimum value for the coefficient gets smaller and smaller. Also, important to note is that the graph is still smooth.

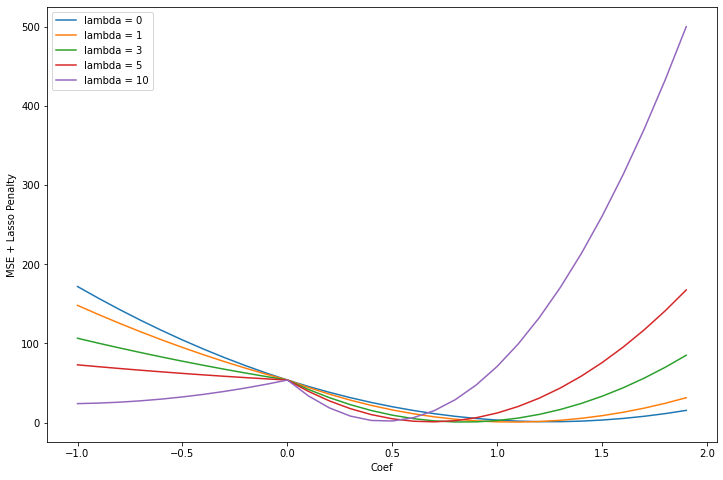

Lets see what happens when we do this with Lasso Regression.

plt.figure(figsize = (12, 8))

for lam in [0, 1, 3, 5, 10]:

mse = []

for i in np.arange(-1, 2, .1):

mse.append(mean_squared_error(df['y'], df['x'] * i + (lam * np.abs(i))))

plt.plot(np.arange(-1, 2, .1), mse, label = f'lambda = {lam}')

plt.legend()

plt.ylabel('MSE + Lasso Penalty')

plt.xlabel('Coef')

Text(0.5, 0, 'Coef')

We notice there is a pronounced kink at 0. This is caused by the absolute value term from the lasso penalty. As the lambda coefficient gets larger, it gets more pronounced. Lets see what happens if I choose even larger values for lambda.

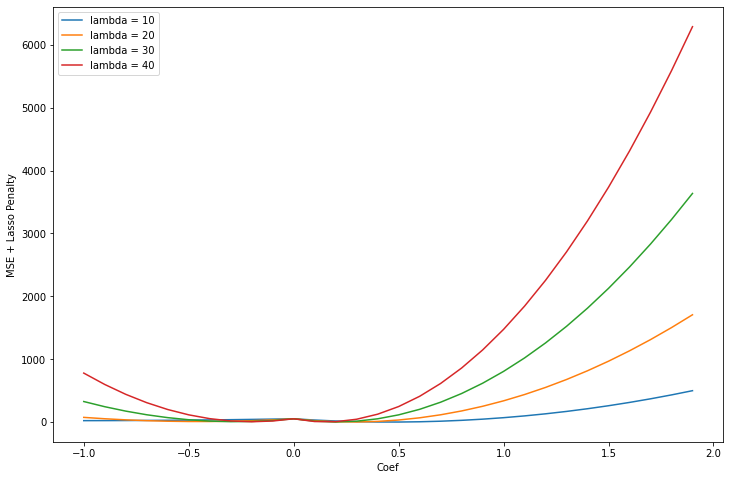

plt.figure(figsize = (12, 8))

for lam in [10, 20, 30, 40]:

mse = []

for i in np.arange(-1, 2, .1):

mse.append(mean_squared_error(df['y'], df['x'] * i + (lam * np.abs(i))))

plt.plot(np.arange(-1, 2, .1), mse, label = f'lambda = {lam}')

plt.legend()

plt.ylabel('MSE + Lasso Penalty')

plt.xlabel('Coef')

We see that the kink at 0 ends up being very near the optimum value for the coefficient.